I have an opportunity worked for Chinese Ministry of Commerce with ICRAF last fall, and have been studying natural rubber value chain since then. I led four technic reports on natural rubber value chain: the first report is for Thailand natural rubber value chain (please see the title);the second one is about natural rubber value chain, foreign investments and land conflicts in Cambodia; the third report is the a comparison study between Thailand and Cambodia, the biggest natural rubber producer and the emerging rubber producer; the last report will concentrate on the risks of natural rubber cultivation and investment in Asia, from geosnatially perspectives. As I mentioned in the reports that there are no winner in the natural rubber value chain: we lost biodiversity and ecosystem services from covering natural forests to rubber monoculture (upstream of the value chain); and emitted million tons of polluted air and water, and carbon dioxide back to nature from rubber processing (the midstream); at the end, without sustainable livelihood for the poor who grows rubber; and limited competitiveness in the end products market (the downstream). We should go back the source and really think about how we can improve the whole value chain, and why.

The following content is the abstract of Thailand report in English. These reports are in Chinese recently, if you are interested in the content please contact Dr. Zhuang-Fang Yi, geospatialanalystyi@gmail.com and yizhuangfang@mail.kib.ac.cn.

Figure 1. The great Mekong region and also the global nature rubber producers.

Asia supplies 93% of natural rubber demand globally. As the world No.1 natural rubber producer, Thailand has exported nearly 40% of global rubber production demands, which is 87% of its domestic rubber production. The production improvement in Thailand is not only depending on its biophysical suitability of rubber growing, but also relying on its policy supports and subsidies to millions of upstream rubber farmers. Thailand has spent about 21.3billion Baht (586million USD) from Sep. 2013 to Mar. 2014 to subsidize its rubber farmers while the price of natural rubber went down. However, lack of manufacturing and financial supports for its midstream and downstream of the natural rubber value chain, Thailand highly depends on rubber exporting to other countries, e.g. China, US, EU and Japan.

The long history of natural rubber cultivation and supports from Thai government has grown Thai rubber farmers a better rubber economic resilience cultivation systems, which is rubber agroforestry. Rubber agroforestry is a rather complex intercropping system compare to rubber monoculture. Rubber monoculture refers to the rubber plantations that only have rubber trees, and other plant species has been killed and get rids constantly by using herbicide and manual clearance. Rubber agroforestry sustains better ecosystem services and also bring more economic returns. But the labour requirement and knowledge gaps from rubber monoculture to rubber agroforestry are the main constrains for a greener cultivation system. It means rubber farmers only need to intensively take care rubber trees in rubber monoculture system, but need other knowledge and time inputs for rubber agroforestry. However, there are about 21 intercropping systems and more than 300 farms are practicing the intercropped rubber agroforestry by the rubber famers without authority supports like rubber monoculture in Thailand. Urgent research and institution support are need for rubber agroforestry in Thailand and globally.

The merging economies and natural rubber producer countries, e.g. Vietnam, Cambodia, Laos, and Myanmar in Mekong region, are following Thailand’s foot steps, only practicing rubber monoculture, that highly support its upstream value chain but lack of rubber manufacturing and supporting financing systems for mid-stream and downstream. It leads to heavily depend on Chinese and the rest of world rubber demands. It leads to very weak economic resilience for millions of smallholding rubber farmers when the price goes down. In China market, rubber price dropped from 6.3USD/kg to less than a dollar in 2014. China, as the biggest natural rubber importer, consuming nearly 40% of global rubber supply. On the other hand, 20% of imported taxes are charged and have dramatically increased the cost of rubber end products, and loss its global competitiveness in the natural rubber market. There are no winner in the natural rubber value chain: we lost biodiversity and ecosystem services from covering natural forests to rubber monoculture (upstream of the value chain); and emitted million tons of polluted air and water, and carbon dioxide back to nature from rubber processing (the midstream); at the end, without sustainable livelihood for the poor who grows rubber; and limited competitiveness in the end products market (the downstream). We should go back the source and really think about how we can improve the whole value chain, and why.

While more and more Chinese state-owned and private enterprises follow “Go Global” strategy by Chine central government who have heavily invested outside of China. Natural rubber end products, especially tires industry is one of them. In this reports, we scrutinized the natural rubber value chain in Thailand and its foreign investments , especially Chinese investments. We tried to answer:

- If there are the best rubber cultivation systems that combine economic returns and a better ecosystem services supporting system;

- The relationship between Chinese investors and Thai natural rubber value chain;

- The possible ways of sustainable and responsible rubber cultivation and investment.

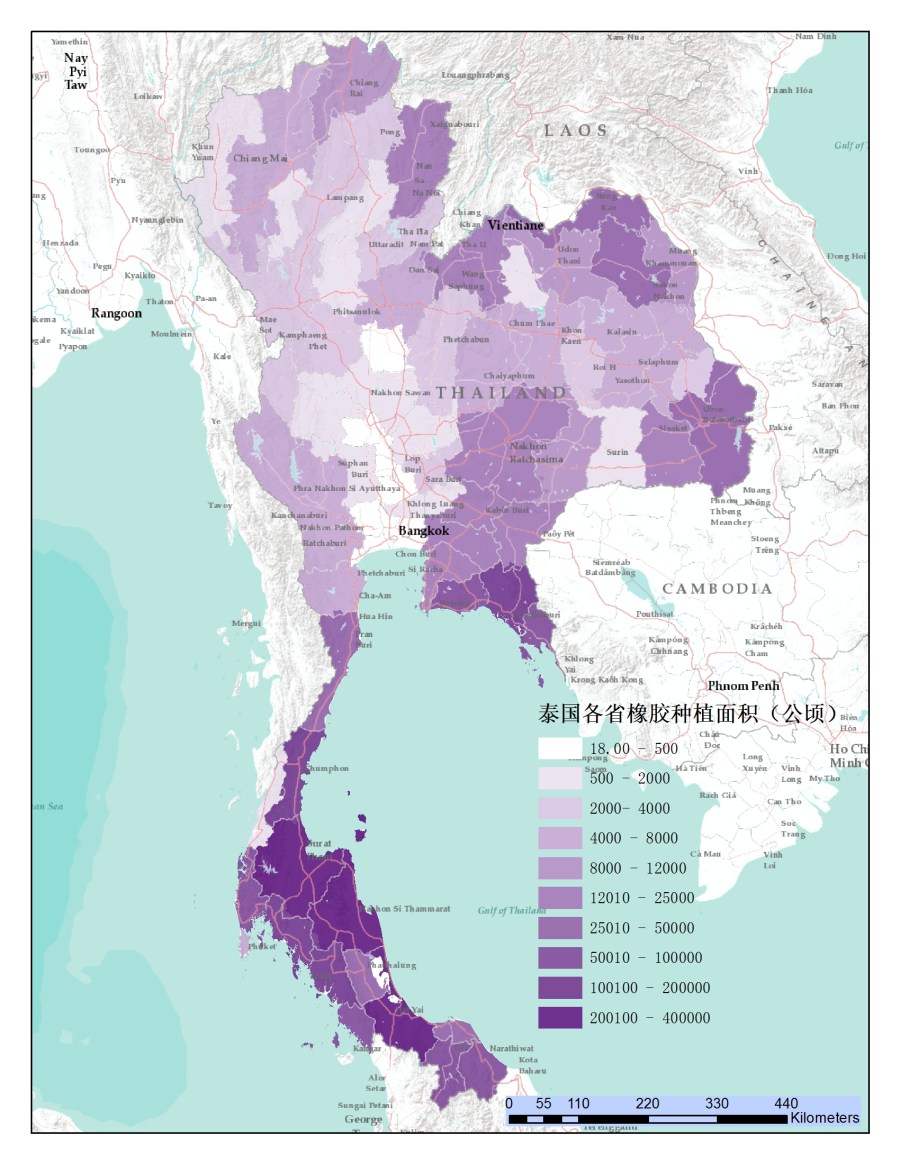

Figure 2. Thailand as the biggest rubber producer, produce 4.5millions ton of natural rubber, and 80% of Thailand domestic natural rubber is from Southern Thailand. Each polygon represents of a province in the map and the darker of the color represents the bigger area of rubber cultivation.